There’s something almost magical about the bankruptcy process. The moment I dropped the “B-word,” collection agencies and their incessant calls went poof—like a genie granting my wish for silence. Dealing with collection accounts in bankruptcy became less of a David versus Goliath affair and more like sending pesky flies away with the swat of a legal hand.

Imagine Mary Poppins but for debt—the court waves its judicial wand, and just like that, debt discharge in bankruptcy sweeps away what I owe. But, as we all know, sometimes the magic doesn’t quite catch, and a bold collector sneaks in a “How do you do?” If that happens, I’m prepared to shout from the rooftops that I’m untouchable thanks to my bankruptcy filing.

And let’s talk about the aftermath. After the dust settles from my creditors’ stampede to escape discharge, there’s that one lender—the ninja waiting in the shadows with a grudge against my car. It turns out, there’s fine print that lawyers like to debate over during brunch, where collection agencies and bankruptcy proceedings collide in a dance over who gets the wheels.

So, pour yourself a cup of knowledge, and let’s enjoy this no-holds-barred ride through the bankruptcy rodeo—I’ll share the good, the bad, and the “you’ve got to be kidding me” moments of bending debt to my will!

Key Takeaways

The very mention of bankruptcy sends collection agencies packing—or it’s supposed to, at least.

A discharged debt is like a superhero’s shield against collectors’ darts.

Your car might still be in hot water, so chat with your lawyer before throwing in your keys.

Collection agencies, you’ve been served—by the court, not me, so direct your calls there.

Remember, repossession rights might still be on the table post-discharge; keep that lawyer on speed dial.

Sample letters to debt collectors can be your script for when they try to improv their way back into your wallet.

Bankruptcy injunction is my “keep out” sign—trespassers will be legally dealt with!

The Initial Shock: Debt Collection Meets Bankruptcy Filing

When I first swung that gavel on my financial woes and declared bankruptcy, I felt like I was striking back at the legion of debt collectors. The automatic stay in bankruptcy, my newfound cape, made me feel like a fiscal superhero. As soon as the bankruptcy papers were filed, the collectors’ grips on my phone line loosened. You could say, it was an instant silence so golden, that I almost wanted to frame it.

But it’s not all about the cape and the cool superpowers, is it? It’s about knowing how to use them. My next move was informing creditors of bankruptcy with confidence that could make a lawyer blush. My spiel? “Talk to my attorney.” It rolled off my tongue like a well-rehearsed line from a blockbuster movie. Every date and every legal term was etched in my mind, ready to be deployed like a verbal boomerang against any debt collector response to a bankruptcy filing that dared come my way.

Collector’s Action

My Response

Outcome

Attempt to call

Invoke automatic stay

Instant peace and quiet

Threaten legal action

Inform of bankruptcy filing

Collector stands down

Persistent attempts

Refer to attorney

Collector redirects efforts

Ignore court injunction

Legal action consideration

Collector potentially faces sanctions

Checking my Google reviews became a habit, almost like sipping on morning coffee while watching the sunrise. The dramatic change in my interactions with debt collectors? Absolutely five-star-worthy. These reviews weren’t just rants of a disgruntled debtor; they were triumphs over those who underestimated the binding magic of a bankruptcy filing.

Staying ever-vigilant became my mantra because, let’s face it, bankruptcy might repel debt collectors like garlic to vampires, but there’s always that one collector who thinks they’re immune. They test the waters, perhaps by sending a sneaky email or leaving a voicemail thinking they can flout the court’s powerful injunction. Little do they know, my legal arsenal is locked and loaded, and my aim is true.

So here I am, basking in the silent symphony of stopped collections and watching with amusement as the gears of bureaucracy turn. My bankruptcy journey may be underway, but the only collection I’m interested in now features zeros in my debt column and a priceless peace of mind.

Navigating the Murky Waters: Collection Agencies During Bankruptcy

Ah, the vast ocean of bankruptcy, where the waters are choppy and the creatures below are just waiting to tug on your financial lifelines. Yet, there’s a beacon of hope, a shining lighthouse that cuts through the fog—the discharge order. This radiant document pulsates with the power to silence creditor harassment with a stern, judicial “Shh!” It’s legally binding, folks! As commanding as a captain on his ship, it orders collections to batten down the hatches and cease-fire.

It’s supposed to be simple: The bankruptcy court orders are served, and the relentless storm of debt collection calls should calm to a serene sea of tranquility. But let’s be real—some collection agencies are like barnacles, steadfastly clinging on despite the current. These determined—or perhaps misguided—entities that choose to scuttle in dangerous waters, trying to collect on debts disallowed by the court, could awaken a Kraken of legal repercussions.

And what of the occasional jingle of my phone or the ghostly whisper of an email notification? Could it be a debt collector breaching the peace of my bankruptcy bubble? Usually, a single, lonely ring is an honest mistake—after all, even Captain Hook could misread his treasure map once. But if the calls continue, if the emails persist? That, my friends, becomes the drumbeat of an impending legal skirmish. This is no mere splash—we’re talking full-on cannonballs of legal countermeasures aimed at stopping debt collection in bankruptcy once and for all.

Now, while most debt collection activities dissolve faster than salt in this bankruptcy sea, there are a few species of debt sharks that still circle my boat. They have their teeth sharpened for the non-dischargeable debts and any fresh credit lines I might have accidentally chummed the waters with after my filing. Watch out, they’re sneaky. But armed with my discharge decree and the vigilant eyes of my attorney, I’m steering this ship toward the calm horizon of financial recovery.

Creditors who ignore bankruptcy discharges get hooked in legal nets

Discharged debt—a siren’s song that halts creditor harassment

A debt collector’s mistake, forgiven once; a storm of calls, bring it on!

Non-dischargeable debt and post-petition credit? Debt sharks be lurking

Financial recovery—my treasure map leads to lands unspoiled by relentless creditors

With every wave that crashes against my hull of bankruptcy protection, I’m learning to navigate these waters like a seasoned captain. And as for those collection agencies that think they’ll pry gold from this pirate’s hold? Well, the discharge order’s got my back, and the silent symphony of ceased collection calls is the only tune I’ll dance to. Anchors are entitled to smoother financial tides ahead!

The Role of Collection Agencies in Bankruptcy

Bankruptcy – it’s that big red stop sign for debt collection agencies, telling them it’s time to take a time-out. Or at least, that’s the theory. When I filed for bankruptcy, it felt like unleashing a superpower. The debt collection agency’s impact on bankruptcy was supposed to be straightforward: cease and desist, retreat and await fate. Some got it right, but others? Let’s just say they treated the new rules like suggestions rather than responsibilities.

I witnessed the wild tango of collection agency responsibilities in bankruptcy firsthand. Their role? About as clear-cut as mud in a swamp – at least to those who fancy themselves above the law. The courtroom became my coliseum, the discharge order my lion, and I, the gladiator, ready to defend against any collector who dared step into the ring post-discharge.

But, just when I thought the battle was won, the rogue collection agency, like a villain in a summer blockbuster, emerged from the shadows. Despite the discharge order blaring like sirens in their ears, these agencies seemed to suffer from selective hearing. Thinking themselves sly, they tested the waters, nudging me with their “friendly reminders” and “just checking in” messages, hoping perhaps to find me unguarded.

Oh, but bankruptcy court didn’t leave me defenseless. Collection agency compliance in bankruptcy isn’t optional, and when they stepped out of line, I was ready with a quiver of legal actions, ready to protect my newly won peace. A legal sword, if you will, forged in the fires of financial reform, to strike down harassment from any collection agency still lurking in the dark corners of debt.

Action by Collection Agency

Required Compliance in Bankruptcy

Consequences of Non-compliance

Harassing phone calls

Cease immediately upon notification of bankruptcy filing

Potential sanctions and legal action

Sending letters or emails

Stop all correspondence related to discharged debt

Legal repercussions, including fines

Not updating credit reports

Report discharged debts accurately as $0

Disputes filed under the FCRA with possible damages

Ignoring bankruptcy discharge

Adhere to the discharge injunction

Penalties and attorney’s fees awarded to the debtor

Yeah, I strutted through the fallen columns of my financial ruins, the shining shield of bankruptcy discharge in one hand and the dark ink of the court order staining my foes. The path ahead was clear of the debt vultures, and the weight lifted felt like skipping through fields in an advertisement for freedom itself. Sneaky collectors heed my warning: bankruptcy is my financial emancipator, and I’ve got the court’s number on speed dial.

Think collection agencies throw in the towel after you file for bankruptcy? Please. They’re plotting like a high-school clique before prom, ready to unfurl their collection agency strategies in bankruptcy with the quiet intensity of a chess grandmaster. Some agencies act quicker than a ninja in a silent movie, thinking they’ve caught me napping post-bankruptcy. They ring up, hoping chaos has clouded my judgment. “Checkmate,” they whisper, but I’ve got the perfect slap-down: “Talk to my lawyer.”

But wait, there’s more. Those pesky creditors with their post-bankruptcy collection tactics, are the ones who slip past the gates, guns blazing with phone calls, eager to re-engage in their favorite pastime: harassment. What’s my response to these die-hard collection stars? A firm and resounding “Nuh-uh!” backed by the steely resolve of legal consequences. Facing creditor actions after bankruptcy discharge isn’t for the faint of heart, but I’m no damsel in distress; I’m the hero in my own financial fairytale.

Now let’s get down to the nitty-gritty—how these collection desperados try navigating the post-bankruptcy landscape:

Creditor Tactic

My Defensive Play

Expected Outcome

Phone call barrage

Invoke attorney communication shield

Collector redirected to legal counsel

Threatening letters

Deploy discharge documentation

Collector retreats to shadowy corners

Inaccurate credit reporting

Assert my FCRA rights for accurate reporting

Collector amends records, lickety-split

Sly legal moves

Mount counter-legal broadside

Collector faces the judicial music

As for those who think they’ve cornered me for the final showdown, think again. My credit report is my castle, and ensuring its ramparts reflect my discharged-debt glory is a potent post-game strategy. Each entry should sing my financial freedom with a “Discharged in Bankruptcy” chorus so sweet, it makes the credit bureaus weep.

So, dust off those collection agency strategies, dear agencies, but remember: I’ve got a bankruptcy shield, legal saber, and an accountant’s precision. Your post-bankruptcy maneuvers are just a high-stakes game, and I’m playing to win. Check and mate.

Legal Repercussions for Collection Agencies Ignoring Bankruptcy Discharges

Oh, to be a fly on the wall when a debt collector, gung-ho and high on persistence, decides to gallop over the line despite a loud and clear bankruptcy discharge. It’s like watching a toddler test the limits of a new babysitter, only with legal consequences that pack more punch than a time-out corner. What’s the first line of defense when facing these knights-errant of the collection world, boldly violating the automatic stay? I pull out the bankruptcy banner, with all the drama of a medieval herald, to remind them of the magical force field protecting my financial castle.

Should the gallant collection agency continue jousting with my peace of mind, they stumble into the colosseum of bankruptcy’s automatic stay consequences for creditors. Trust me, it’s not the kind of fame they’d want. The bankruptcy court doesn’t take kindly to creditors’ violation of bankruptcy injunction, treating their willful fits like a matador treats a bull’s charge—with swift, decisive action. Let’s just say that the agency that dares step into the ring, they aren’t just facing a stern wag of the finger but could also be coughing up some serious dough for my attorney’s fees, and fines that make their own coffers weep.

I can almost hear the gasp of the audience as the collector, brazen as a Shakespearean villain unaware of the poisoned goblet, strides into a lawsuit’s trap. It’s a moment of poetic justice when the Fair Debt Collection Practices Act and the Fair Credit Reporting Act unfold like twin scrolls, outlining in no uncertain terms that my discharged debts are as untouchable as a dragon’s hoard. For the debt collector bold enough to knock on my drawbridge, they are greeted with the full spectacle of legal repercussions. This isn’t mere money-changing hands; it’s a lesson in the high art of ‘don’t mess with bankruptcy discharge’, and I’m here for the drama.

FAQ

What should I do if a collection agency continues to report my discharged debt?

If a collection agency keeps chanting your old debts’ names like a broken record, it’s time to cut the track. Inform the credit bureaus that those debts are discharged, and then consider striking back with legal action. Collectors should update your credit report to reflect your debt-free glow-up so you can strut into your financial future with no baggage.

What legal actions can I take if a debt collector ignores my bankruptcy discharge?

If a collector trips over the line even after your debts have danced into the sunset (aka discharge), they’re in the hot seat. You can wave your discharge papers and remind them it’s game over. If they keep pushing, a lawsuit might be your next victory dance, making them pay for their boldness – and possibly your attorney’s fees, too.

Are there ways to counter collection agency strategies after bankruptcy?

Oh, absolutely. Strategy Numero Uno is: Keep your attorney on speed dial. They’re like your knight in shining legal armor against rogue collectors. Strategy Deux: Keep your paperwork fortress in order. This way, if they attempt to slyly collect, you’ve got your arsenal of documents to defend your financial realm.

How might a collection agency react to my bankruptcy filing, and what should I watch out for?

Once you’ve made the bankruptcy move, some agencies might try to regroup and come at you with legal loopholes or prey on confusion. Stay frosty, and be ready to deflect any sketchy moves. Remember, the bankruptcy filing is your queen on the chessboard, so use it to protect your kingdom from their sneaky checkmates.

How do I ensure collection agencies are abiding by the rules during my bankruptcy case?

Staying on top of your bankruptcy filings and communications is key. If a collector steps out of line, you’ve got the power to report them to your attorney or the bankruptcy court. The Fair Debt Collection Practices Act (FDCPA) is also your BFF here, ensuring agencies play nice, or they risk getting benched – legally speaking.

What happens if a collection agency decides to collect on a debt after I’ve filed for bankruptcy?

If they dare to do the collection dance on a debt that’s now in bankruptcy’s hands, they could be breaking the law. Collection agencies are expected to cease all collection endeavors, or they might get slapped with fines – or worse. If this happens, tell them to talk to your attorney, who will not be happy to see their number on caller ID.

Are there any debts that are immune to the automatic stay’s protective bubble?

Yes, not all debts get to join the ‘automatic stay’ party. Certain debts like child support payments, some taxes, and student loans often sashay right past those bankruptcy velvet ropes. If you owe on those kinds of debts, expect collectors to keep knocking. The bankruptcy court spells out which debts are the wallflowers still open for collection business.

What if collectors are still hounding me after filing for bankruptcy?

If collectors are acting more clingy than a sock out of the dryer after you’ve declared bankruptcy, it’s time to pull out the big guns – and by that, I mean legal protection. Annoying calls should be promptly reported to your attorney or the bankruptcy court. These zombie debt collectors can face consequences if they don’t respect the court orders designed to stop collection actions.

Can debt collectors still contact me once I’ve filed for bankruptcy?

In theory, no. The automatic stay in bankruptcy is like wearing an invisibility cloak around collectors. However, some might have missed the memo or play dumb, trying their luck. If that happens, just repeat your bankruptcy mantra, provide them with your case number, and remind them to bug your lawyer instead.

What is this ‘automatic stay’ I keep hearing about, and will it stun my debt collectors into silence?

Yep, the automatic stay is basically your financial force field. Flip that switch by filing for bankruptcy, and collection agencies should freeze like a game of Red Light, Green Light. It halts all harassment from debt collectors faster than you can say “moonwalk.” Just be sure to inform them of your new untouchable status so they don’t accidentally (or “accidentally”) keep the pressure on.

How do I get debt collectors to back off after I’ve filed for bankruptcy?

You simply serve them the bankruptcy card. Tell them you’ve filed, and like vampires facing garlic, they’re supposed to skedaddle. They need to take any beef regarding your debts to bankruptcy court – not your doorstep. If they’re still not getting it, loop in your attorney, who can lay down the law in style.

What’s the deal with my collection-llama drama after filing for bankruptcy?

Oh, it’s like a cease-and-desist for their relentless spit-storm. Once you file for bankruptcy, an “automatic stay” kicks in faster than you can say “no más,” and debt collectors have to put their collection antics on pause. Any debts that were in the midst of a collector’s samba are included in the bankruptcy process, which could lead to a debt discharge in bankruptcy, washing those debts clean. Until then, if they ring you up, remind them you’re under the bankruptcy court’s wing now, and watch them scatter!

Let’s face it, navigating the choppy waters of utility bills during bankruptcy can make surviving a five-year reality TV-esque divorce drama look like a cakewalk. But here’s the scoop: Chapter 7 bankruptcy has become my newfound hero, swooping in to keep the essentials like electricity, gas, and even my endearingly archaic landline phone running smoothly—despite a history of payment slip-ups. The best part? Once you’ve declared bankruptcy, those utility companies must keep your services flowing as if you’re royalty, even though your pockets are echoing. And for those of us with an emergency on our hands (every utility bill feels like a ticking time bomb, am I right?), an emergency petition could be your knight in shining armor—buying you 14 precious days to get your paperwork act together.

But don’t just take bankruptcy’s hand without considering a dance with utility discount programs first; you might find a partner that doesn’t lead you around in circles. Now, if we’re talking cable TV, prepare for a plot twist. That’s the diva of utilities—no red-carpet treatment there. It’s not covered by the bankruptcy shield, so stay up to date or get ready to miss the season finale. We’ve got to weigh our options, folks, like choosing between eating leftovers for a week or facing the wrath of a shut-off notice.

So put on your utility management hat (yes, it’s a thing), and let’s figure out this whole managing utility bills in bankruptcy conundrum together—and keep those lights on!

Tackle an emergency petition with urgency—it’s your 14-day utility grace period.

Utilities are royals in the land of bankruptcy but don’t expect the red carpet for cable TV.

Utility discount programs and assistance may offer easier paths than bankruptcy.

Remember: bankruptcy or not, it’s essential to stay current on utility bills during bankruptcy.

Utility Bills During Bankruptcy:

Whoever said “let there be light” probably wasn’t drowning in utility bills during bankruptcy. But for those of us embarking on this financial odyssey, keeping our utilities running during bankruptcy is like trying to juggle with one hand tied behind our back—challenging, but not impossible. So, allow me to illuminate the unlit path of staying connected with utility bills in bankruptcy.

Lesson one in bankruptcy school: if your bankruptcy schedules miss the part where they say “Psst, you owe on utilities,” that’s a party foul. It’s the equivalent of forgetting to invite your electric company to the money-forgiveness party and rest assured, they will hold a grudge, resulting in a dark, silent abode for you.

Remember, owing money for that precious electricity and water before you declare bankruptcy is like having a bad rep—it sticks. But once you file that paperwork, you’re in the clear with the old stuff (phew!). However, don’t start thinking it’s all easy street from here. Any new utility bills during bankruptcy mean you’re whippin’ out the wallet. Bankruptcy might wipe the slate clean, but it won’t warm your shower water.

And what’s this “adequate assurance” business? Sounds like something my therapist would say. But no, you promise that your post-bankruptcy self will be a better bill-payer. You get a 20-day countdown to strut your stuff and prove you won’t leave your utility company high and dry. A letter, some cash, a solemn vow—I don’t know, get creative. But deliver on this. Otherwise, expect service interruptions like your favorite show being cut off at the season finale cliffhanger.

But wait, there’s a plot twist. If you still find yourself taking a candlelit bath—not by choice—your next stop shouldn’t be the bar; it should be the courthouse. Waving the white flag of paperwork might just reignite those home hearths—or at least get the utility company off your back.

Rule #1: No utility bill on your bankruptcy schedule is like forgetting your keys—it’s a surefire way to lock yourself out of power and water.

Rule #2: Like a strict diet, bankruptcy demands you only chew on new debts—pay those fresh utility bills or face the shut-off music.

Rule #3: “Adequate assurance” is not a wink; it’s a solid, financial pinky promise. So show your utility provider the money—or at least, say you will.

Rule #4: Should the lights go dark, it’s not time for ghost stories—sprint to that bankruptcy court and get your service back faster than a reality TV star’s career revival.

Now you’re equipped with a beacon of knowledge in the dark tunnels of bankruptcy utility bills. May your days be bright and your showers warm as you navigate these murky waters.

The Odd Case of Cable TV in Bankruptcy

Amid the swirling whirlpool of bankruptcy and utility bills, cable TV stands out like the awkward guest at the superhero soiree. It’s not that it’s an uninvited pest—more like it didn’t get the same RSVP as the others. Here I was thinking my small screen addiction could sneak through unscathed in a bankruptcy saga, but turns out, the cable folks can cut the cord on my zombie marathons quicker than I can say “apocalypse.”

What’s the deal? In the grand theatre of bankruptcy, utilities are the A-listers with front-row tickets. Miss a payment, and with a bankruptcy claim, you might still keep the lights on. However, in the green room, cable TV’s prima donna attitude makes it exempt from these cushy protections. Sure, you might clear the slate of past-due charges, but that doesn’t mean you get to keep up with the Kardashians if the current bill goes unpaid. It’s like after the bankruptcy confetti lands if you can’t pitch in for the clean-up, cable’s not hanging around.

So, it boils down to this—you could wipe your TV debt clean when the bankruptcy credits roll, but when the next season is queued up, you’d better make sure your cable account is feeling the love, or else it’s nighty-night to your nightly news.

One could argue, “but my binge-watching needs!” to which I’d respond, “brace for reruns.” If utility bills in bankruptcy are a game of thrones, cable TV demands you pay tribute to stay in the realm, bankruptcy badge or not. Therefore, it might be wise to plant your financial roots in more fertile ground—keep up with those cable bills to stay connected.

So my fellow sitcom soldiers and reality TV renegades, while bankruptcy might be the noble steed that rescues your utilities when it comes to cable TV—get ready to duel with your checkbook. Your armor against an abrupt blackout? A timely payment, lest your living room be thrown back to the dark ages (or at least the 1990s). In short, manage those utility bills in bankruptcy like a budgeting ninja, and maybe, just maybe, you’ll survive this episode unscathed.

Utility Bills in Bankruptcy: Staying Connected

There’s a fine art to managing utility bills in bankruptcy, and it’s about as straightforward as trying to fold a fitted sheet. It gets even trickier when you throw bankruptcy utility bills into the mix. Imagine Chapter 7 bankruptcy as that friend who helps you sneak into the movie theater—once you’re in, your overdue utility debts disappear like my commitment to a low-carb diet. On the other hand, with Chapter 13, think of your debts packed tighter than a can of sardines into your repayment plan.

But be warned, the struggle doesn’t end there. Keeping staying connected with utility bills post-filing is like being on a reality show—you’ve got to play the game. Keeping up with current bills is your ticket to uninterrupted showers and binge-watching sessions during those repayment years. And trust me, that utility company has less patience than I do when my Wi-Fi drops out mid-season finale. So let’s not test them, shall we?

It’s like doomsday prepping—but for your bank account. Say you’ve operated on a diet of candlelight and cold leftovers thanks to dreaded utility shut-offs—Chapter 7 could be your savior, and Chapter 13, while more of a tough-love approach, still gets you through the nuclear winter of debt. The real question is, can you keep the torch burning after the bankruptcy storm has passed? Rest assured, friend, those utility bills will keep coming, relentless as a telemarketer during dinner time.

Bankruptcy utility bills might seem like a ghastly goblin you’d rather not face, but the payoff is sweeter than Halloween candy. If you want to keep the lights on and avoid horror-movie vibes at home, it’s simple—get snug with your payment plans and show those utility bills some love. Because if you don’t, you could find yourself back in the dark, and not just figuratively speaking.

With Chapter 13, pack those overdue utility bills into your repayment luggage.

After your bankruptcy declaration, new utility charges are your new frenemies.

Stay current on those utility bills, or risk going back to the stone ages—electricity-wise, that is.

I’ll tell you this much—managing utility bills in bankruptcy requires a keen eye and the delicate balance of a tightrope walker—and that’s why I’m learning to juggle these financial obligations like a circus pro. With a little finesse and a playbook of rules, I’m keeping that shower hot and the Netflix streaming and you can too.

When Your Utilities and Bankruptcy Collide

Picture this: you’re knee-deep in bankruptcy utility bills, cozied up with your microwave popcorn, ready for the next episode of your life—then bam! Your favorite show stops mid-cliffhanger. It’s the ultimate showdown, utility bills during bankruptcy versus the will to keep watching. Lucky for you, I’m your guide on this reality TV-worthy escapade of staying connected with utility bills while the bankruptcy credits roll.

Sure, I’m no knight in shining armor, but I’ve got some tricks up my sleeve that can keep your utilities running smoother than my last date. Think of programs like LIHEAP and utility discount programs as your financial fairy godparents—they sprinkle a little magic dust on those pesky past due notices, preventing your heat from going as cold as my ex’s heart in winter.

Of course, when the going gets tough, and the funds are low, doling out payments over time seems like a dreamier plot than any rom-com’s happy ending. But it’s not all about the short-term fix; let’s think big picture. We’re talking about leveling out those steeper-than-a-roller-coaster utility bills with an average billing plan, because who needs more surprises?

Listen, I’ve been through the wringer, so believe me when I say a little energy conservation goes a long way—the same way constructing the perfect online dating profile does. You’ll thank yourself when you’ve got extra cash for a stress-relief spree because nothing soothes the soul like a venti triple-shot espresso after a day of number-crunching and soul-searching, right?

It’s time to whip out the big guns and map out your game plan. Want a preview? Here’s a table with some insights that even the savviest of reality show contestants could use:

Program/Assistance

What It Does

Long-term Benefit

LIHEAP

Helps manage heating costs.

Avoids utility shut-off during bankruptcy’s winter season.

Utility Discount Programs

Offers reduced rates based on income.

Keeps your bills affordable, like budgeting for coffee after kicking luxury habits.

Average Billing Plans

Spreads out high usage costs throughout the year.

Prevents sky-high bills and prevents heart attacks from unexpected charges.

Energy Conservation Assistance

Offers free or low-cost tips to reduce usage.

Slashes bills. Now you can splurge on those fancy LED bulbs—or another round of trivia night.

So, as you arm yourself with the power of knowledge (and your remote control), remember this: bankruptcy doesn’t have to mean the end of Netflix nights or hot showers. With these programs in place, you’re the star of your own comeback story. And heck, if you play it savvy enough, you’ll stay as connected to your utilities as I am to my trusty streaming service—through thick and thin, budget cuts and binges.

And that, my fellow budgeteers, is how you turn an epic showdown into the season finale everyone’s talking about. Who knew that surviving utility bills during bankruptcy could provide so much material for my stand-up act? Throw in a bit of financial literacy, and a dash of resourcefulness, and voila—you’re not just staying afloat, you’re sailing through bankruptcy like it’s the latest adventure series. Now go on, give yourself a round of applause—you deserve it!

Maintaining Services During Bankruptcy Proceedings

So, I’ve decided to see this whole bankruptcy thing as not just a financial debacle but an intriguing game of Monopoly where I’m dodging the ‘Go to Jail’ square. But instead of jail, it’s my utilities on the line, hanging by the thread of my pocketbook’s kindness. It’s like I’ve landed on the ‘Electric Company’ and, ladies and gents, I’m rolling the dice—I need to make some sharp moves to avoid blackouts in my very own living room.

The thing about managing utility bills in bankruptcy is that it’s a delicate tango between you and your utility provider. The name of the game here is “adequate assurance,” a fancy way of saying, “I promise I’m good for the cash, cross my heart, and hope to cry in the dark.” And the clock’s ticking—I have to showcase my most responsible self within 20 days through a letter of credit, a chunk of my savings, or a pinky promise fortified with a notary seal; whatever floats the utility company’s boat.

But what if my utility provider’s giving me side-eye, doubting my good intentions? It’s as if my assuring smile and batting eyelashes when promising to pay aren’t worth a dime. Well, my friends, it’s time to turn to the one person who can mend this impending domestic blackout—Judge Judy or whoever’s wearing the robes in bankruptcy court.

Picture this: I’m pleading my case, armed with my most charming “trust me” eyes, as I make an impassioned plea for reasonable security deposits. Because, let’s be real, the suggested amounts make my wallet weep and have me fantasizing about inviting the town over for what I’d only half-jokingly call the “bankruptcy bash”—BYOC (bring your own candle).

So, here’s an insightful table on what happens when staying connected utility bills clash with the heavyweights of bankruptcy utility bills. It’s a gritty saga of post-dated promises against real-time payments, and I’m the hero of this quirky financial drama!

Your Move

Utility Company’s Counter

Final Duel With the Judge

Provide a Letter of Credit

Potential Side-Eye, “Is This Legit?”

“Your Honor, I am good for it!”

Make a Cash Deposit

May Request a Golden Scepter as Collateral

Bring Receipts, You Might Just Win

Flash a Surety Bond

“Hmm, Our Risk Department Will Sleep On It”

An Offer They Can’t Refuse? Challenge Accepted!

Show Some Prepayment Action

Preferred VIP Move—Champagne is Poured

Less Screen Time In Court, More TV Time At Home

The plot thickens as my utility dilemma continues to unfold like a daytime soap opera with less attractive actors. Will I conquer the game and keep those flames burning or stumble into an unwelcome Amish lifestyle?

There’s more to this tale, and trust me when I say it’s not your grandma’s managing utility bills in bankruptcy story—it’s a tale sprinkled with humor, legal jargon, and the quest to keep my digital life thriving amid financial adversity. Stay tuned!

Managing Security Deposits and Utility Services Post-Bankruptcy

Alright, picture this: you’ve just come out the other side of the bankruptcy rollercoaster, feeling a little frazzled but definitely ready to conquer the world again – or at least your living room. Post-bankruptcy life has its unique charm, akin to rediscovering the dating scene after a particularly theatrical divorce. And in this new chapter of financial rebirth, managing utility bills in bankruptcy takes center stage.

You see, post-bankruptcy, there’s this sort of ritual that involves offering up a security deposit to the utility gods to keep or reconnect the lifeblood of modern existence – electricity, water, you know the gang. In some twisted way, it’s not unlike giving your date a good-faith deposit to ensure you won’t ditch halfway through dinner. But here’s where it can feel like the utility company is trying to swipe right on your entire savings account.

If the amount they’re demanding resembles a king’s ransom, remember – bankruptcy court is like your wingman, ready to intervene on your behalf. They’ve got the prowess to negotiate a deposit that doesn’t require auctioning off family heirlooms or dipping into the kids’ college funds. Yeah, that’s right, the court can put its foot down and say, “Let’s keep it reasonable folks.”

But wait, it gets even better. With on-time payments – something I wish I’d learned from marriage the hard way – you might just win a year-long trust challenge. Score that and, presto, you’re reunited with your security deposit like a tearful airport scene in a romcom. It’s like the utility company’s saying “Hey, we trust you again!” Now isn’t that a badge of honor?

Pro tip from someone who’s been through the wringer: while the thought of chatting up utility customer service might give you cold sweats reminiscent of late-night calls with lawyers, it’s your VIP pass to avoiding cold reality showers. Strike up a conversation, explain your situation, and you might emerge both squeaky clean and toasty warm.

Here’s the deal in plain language: when it comes to utility bills during bankruptcy, your swiftness and savvy in handling security deposits could be what keeps your heat humming and your water flowing. Be the maestro of your bills, not the other way around. So go ahead, dial up your utility provider, and politely inquire about rekindling your electric affair post-bankruptcy. It’s either that or get comfortable with candlelit dinners – and not the romantic kind.

Communication Is Key: Talking to Your Utility Provider

Let’s cut to the chase: staying connected with utility bills while quietly drowning in the sea of bankruptcy utility bills is about as much fun as trying to convince my cat to take a bath. But here’s a hot take—communication with your utility provider is more critical than my morning espresso shot on a Monday. Hitting up those customer service lines isn’t just for contesting that “mysterious” charge for premium channels you never ordered—it’s for navigating the utility bills during bankruptcy without your life turning into a horror movie where the lights ominously flicker off.

If you’re roaming the wildlands of D.C., remember, that you’ve got a veritable smorgasbord of customer service numbers and walk-in centers for PEPCO, Washington Gas, and the DC Water and Sewer Authority. Think of them as your utility superheroes, sans the capes and tights—ready to swoop in to discuss your next move before your utility services pull a Houdini on you. These aren’t clairvoyant hotline psychics, but they’re the next best thing for making sure your fight to keep the lights on goes as smoothly as my charm offensive at the last call.

Breathe easy because you’ve stumbled upon an article written by someone who’s been in the trenches of bankruptcy utility bills warfare. So take it from me—picking up the phone might just be the game-changer. No, they won’t whisper sweet nothings or coo comforting life advice into your ear, but they can offer guidance on how to keep your services running without the need for candles (unless you’re into that). It’s about rights, options, and yes, possibly finding a friendly operator who echoes those inspirational posters plastered in high school counselors’ offices about ‘hanging in there.’

FAQ

How do I talk to my utility provider when I’m in the thick of bankruptcy?

Dial that customer service number and charm their pants off. Or at least keep them from cutting off your essentials. Just remember, you’re not confessing your love—you’re convincing them you’re worth the risk. Be honest, be upfront, and who knows, you might avoid that shower shocker.

Post-bankruptcy, will I need to secure my utilities with a hefty deposit?

Probably, but don’t panic. Think of it less as a hurdle and more like a trust fall. You might have to float some cash, but hey, act like a financial saint for a year, and you could get that deposit back. Just avoid making it rain in the meantime.

What happens if my utility provider isn’t convinced by my “adequate assurance”?

Time to lawyer up and head for court! If your utility provider gives you the side-eye and demands more than you can handle, the bankruptcy judge can mediate. It’s like couple’s therapy but for your wallet.

Are there programs that help me with utility bills if I’m filing for bankruptcy?

Yes, some programs can help lighten that load. Check out the federal LIHEAP program or various utility discount programs that work like a financial stress ball, squeezing those overwhelming utility bills into something a bit more manageable.

Help! My cable got cut! Does bankruptcy cover my zombie marathon sessions?

Here’s the deal – cable is the diva of utilities. It’s not guaranteed the same protections, which means your post-apocalyptic fantasies might need to be paused. Cable debt can be discharged, but the power to keep it flowing? That’s a “you” problem.

Can I get assistance for utility bills during my Chapter 13 bankruptcy reorganization?

Yeah, you can. Chapter 13 squishes your delinquent utility bills into your repayment plan but treat those new bills like a Tinder date you want to see again – with respect and timeliness.

What’s this “adequate assurance” I keep hearing about?

In dating terms, it’s not flowers—it’s more like putting a ring on it. After filing, you have 20 days to prove to your utility providers that you won’t ditch your bills. It’s like saying, “Believe me, I’m good for it!” and then having to show receipts. Literally.

Are all my utility bills forgiven in bankruptcy?

Let’s get real. Filing for bankruptcy does to your old utility bills what a woodchipper does to…well, wood. Kaput. However, any charges after your filing? That’s on your tab, pal. Keep your checkbook handy for the current stuff.

Can filing for bankruptcy keep my utilities from being shut off?

Absolutely! Filing for bankruptcy, especially Chapter 7, often comes with a no-shut-off perk for your utilities. Think of it as an “unplug me and suffer the legal consequences” kind of deal. But remember, as with reality TV show cliffhangers, the suspense only lasts so long – you’ve got 20 days to show you can keep up with future bills.

What if I accidentally forget to list a utility bill when filing for bankruptcy?

Oh, you mean play financial hide-and-seek? Bad move. If you don’t list it, you might as well prepare to light candles for a very nostalgic evening. Declare every bill, or risk singing “Baby, It’s Cold Inside.”

When I first waded into the swampy waters of bankruptcy, I couldn’t help but notice how some debts strut around like they own the place. I’m talking about priority unsecured claims in bankruptcy, the financial prima donnas that cut the line and demand attention. Whether it’s for the importance in the bankruptcy process, or just their unforgiving nature, these debts are like the A-listers at an award show, and they’re getting their money bags before anyone else has their photo snapped.

As I chewed through the gristle of understanding priority debts, it became clear that these are not your garden-variety IOUs. Oh no, these are the debts that linger and haunt your financial dreams like an indigestion nightmare. They include the headliners like child support and alimony—always top billing because, oh darling, family comes first—as well as the heavy hitters like criminal fines and freshly baked tax obligations. Just when you thought bankruptcy was your golden ticket, you realize it’s also a VIP list, and your name might not be on it.

As for me and my financial obligations in bankruptcy, we’ve had some awkward dances. You might too. But listen up, because knowing who’s who in this high-stakes paddle game could be just the lifeline you need to hobble on toward a brighter, debt-free dawn.

Key Takeaways

Priority debts are the exclusive club of financial obligations in bankruptcy; they always get paid first.

Grab a ledger and take note: Priority debts include family support, government fines, and recent taxes.

Filing bankruptcy won’t make these elite debts vanish—they’re the stage-5 clingers of your financial world.

Understanding the hierarchy between priority and non-priority debts can make or break your bankruptcy strategy.

Remember, just because bankruptcy opens its doors, doesn’t mean all debts are invited to the after-party.

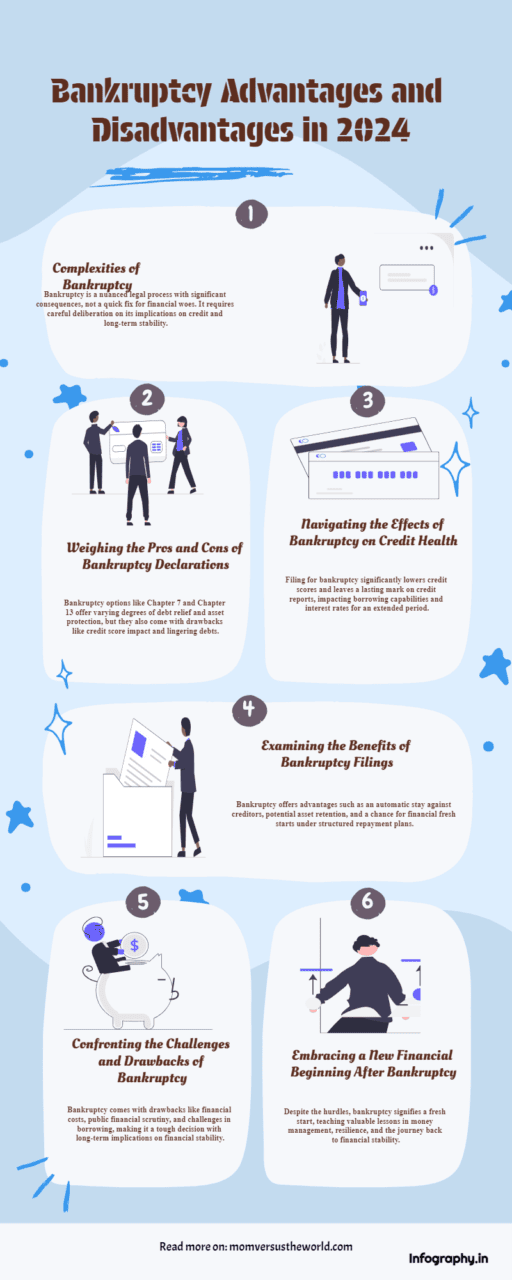

The Lowdown on Chapter 7 and Chapter 13 Bankruptcy

Let me paint you a picture: you’ve hit financial rock bottom, and it’s kind of messy that even a mop advertised in a late-night infomercial couldn’t clean. Your wallet’s thinner than a supermodel on a juice cleanse and creditors are beating down your door. That’s when you consider playing your ace—bankruptcy. But not all bankruptcies are cut from the same cloth. We’ve got Chapter 7 bankruptcy, the liquidation hoedown, where your assets go bye-bye in a buyout to pay off those pesky debts. It’s essentially a fiscal fire sale.

But wait, there’s more! Imagine Chapter 13 bankruptcy, the financial fairy godmother that doesn’t grant pumpkin carriages but does give you something even better—an organized payment plan. It’s like a financial makeover for your debt-riddled life. Instead of offloading your belongings faster than a hot potato, you strut down the runway of reorganization bankruptcy, waving a court-approved repayment plan. It might last a cool five years, but it’s tailored to your pockets. Queue the montage of you, the savvy debtor, mailing out checks to creditors like holiday cards, spreading not joy but installments.

Oh, and don’t forget the stars of the show: the bankruptcy types that get all the attention. Liquidation bankruptcy, a.k.a. Chapter 7, is your quick(ish) escape from debt’s shackles, while reorganization bankruptcy, our friend Chapter 13, is more of a marathon than a sprint, with a compassionate pat on the back that says, “Hey, you got this.” It’s about endurance and playing the long game.

Features

Chapter 7 Bankruptcy (Liquidation)

Chapter 13 Bankruptcy (Reorganization)

Process

Selling of assets

Court-approved payment plan

Duration

4-6 months

3-5 years

Property Fate

Could be lost

Typically retained

Credit Impact

Stays on report for 10 years

Stays on report for 7 years

Debt Elimination

Immediate (upon discharge)

Gradual (as plan is completed)

Best For

Individuals with little to no disposable income

Individuals with regular income and willing to pay back debts over time

So there you have the headline acts: Chapter 7 bankruptcy is your liquidation headliner, razzling and dazzling as it turns your assets into cash confetti. Chapter 13 bankruptcy is more of a behind-the-scenes maestro, orchestrating your payments into a symphony that harmonizes with your fiscal reality. Trust me, knowing the differences between these two bankruptcy types is like knowing if you’re allergic to shellfish before a seafood buffet—it’s crucial for your survival.

Whether you decide to unload your burdens by liquidation or stick it out with a repayment concerto, bankruptcy is more than just financial white noise. It’s the grease in the gears of your economic reboot. Remember, folks, as you slide through the bankruptcy slip ‘n slide, clutch your financial dignity and make a splash that counts.

Priority Unsecured Claims in Bankruptcy: What Are They?

So, let me lay it on you: in the big bad world of bankruptcy, some debts practically strut down the red carpet with more sass than a celebrity at an awards gala. We’re talking about the A-listers that the courts can’t seem to say ‘no’ to. I mean, if your debts were a family dinner, priority debts would be that one relative who always gets the first and juiciest cut of the turkey. Classic.

These VIPs include that chunk of change you shell out for child support, because kids, well, they’ve got to eat. Then there’s alimony, because love might die but the need to keep your ex in yoga classes sure doesn’t. We’ve also got those criminal fines—think of them as societal ‘oopsies’ that come with a price tag—and let’s not forget the IRS priority debts. Oh, the IRS—like that cousin who lent you cash that one time and never lets you forget it.

When the gavel drops and bankruptcy is declared, these priority debts get first dibs on your wallet. And why? Because the law says so! They’re considered so essential that your remaining cash is pretty much theirs for the taking. It’s like a financial ‘Hunger Games’, and these creditors have the best weapons.

Now, friends, don’t confuse these with secured priority debts, which are kind of like the bouncers outside Club Bankruptcy—they’ve got collateral to lean on. Think of your house for that mortgage or your car for its loan. On the flip side, unsecured priority debts don’t have anything to hold hostage. They’re based purely on the promise that you’re good for it, crossing their hearts and hoping to collect.

It’s important to note that even in a Chapter 13 bankruptcy, where it feels like you’re on a financial diet and scrimping every penny, those priority debts need to be paid in full. No shortcuts, no IOUs, and definitely no ‘I’ll get you next time’. They’re like the friend who orders the steak at a split-the-bill dinner. They’re getting their share, and you better believe it’ll be off the top!

Examples of priority debts include child support, alimony, criminal fines, and IRS obligations

IRS priority debts—they want what’s theirs, and they’ve got laws to back it up

Secured priority debts have collateral, while unsecured priority debts do not

In Chapter 13 bankruptcy, priority debts are the divas that demand full payment

So, as you navigate the bankruptcy battlefield, pay homage to the priority debts—they’re your financial overlords, and they will not be ignored. Treat them right, and your journey through debt may just have a sliver of silver lining. Skimp on them, and you’ll find it’s a bit like stiffing the mafia—a definitely unwise career move.

Priority vs. Non-Priority Unsecured Claims

Let’s dive right into the great circus of bankruptcy, shall we? In one corner, we have the high-flying priority debts swinging from trapeze to trapeze with the greatest of ease. And in the other corner? The ground-level grunters, the non-priority unsecured debts, just hoping for a scrap of attention. The way these two are treated in the bankruptcy arena is more lopsided than a three-legged race at a family reunion.

I’ll be the first to say, that priority unsecured claims treatment in bankruptcy is a spectacle you can’t unsee. You’ve got debts that are practically wriggling in excitement like eager puppies because they know they hold a golden ticket—priority unsecured debts. Owe child support? Back of the line. Uncle Sam’s slice of your pie comes first. Tax debts from the federal government are the influencers of the debt world, my friends, unloading their cache of demands with the swagger of a ‘celebrity-endorsed’ by bankruptcy law, and by celebrity I mean because they did a bit more than just influence the law, they wrote it. Can you spell CONFLICT?

Then there’s the riffraff—the non-priority unsecured debts. We’re talking credit card debts wearing yesterday’s fashion, personal loans that missed the memo, and those overdue utility bills lounging like they’re at the beach without a care in the world. Don’t get me wrong, they want their money, but in the hierarchy of debt repayment, they’re basically serenading from the balcony while priority debts are having a private soirée on the main stage.

In the bankruptcy ballgame, these non-priority minnows often end up catching the short straw, making do with dimes on the dollar, if they’re lucky. Think of it like a bake sale where the cupcakes run out just as they reach the front of the line—all the anticipation with none of the sweet payoff.

Priority debts: First-class passengers with a velvet rope and a bouncer.

Non-priority unsecured debts: Coach passengers gazing wistfully past the curtain.

So, what’s the bottom line as we untangle this knotty web? Understanding the difference between priority vs. non-priority debts isn’t just some intellectual hoopla—it’s the difference between who sees green and who gets lean in the bankruptcy showdown. It’s knowing the VIPs from the general admissions in the never-ending carnival that is your financial restructuring. And now, armed with this knowledge, you, my dear reader, can saunter into that bankruptcy courtroom with the confidence of a ringmaster in full regalia.

Tackling IRS and Secured Priority Claims in Bankruptcies

Let me tell you, handling IRS priority debts during bankruptcy is like trying to get rid of that houseguest who’s overstayed their welcome but insists on sticking around for breakfast, lunch, and dinner—and I’m not talking the avocado toast kind. Uncle Sam has quite the appetite, and he’s ready to feast on any assets you might have left. These debts are the wallflowers that somehow end up leading the conga line; they don’t budge until they’ve had their fill. We’re talking taxes here, the kind of obligations that have their own VIP section in the bankruptcy club.

Now, move over to the world of managing secured priority debts. Secured debts – oh, those are the bouncers of the creditor world. You know, the ones that have your car keys in one pocket and your house deed in the other? If you don’t pay up, they’re ready to sweep in and take your treasures on a one-way trip to Auctionville. But here’s a twist: if you’re in the sassy grips of a Chapter 13 bankruptcy, there’s a catwalk you can strut down. It’s called a bankruptcy strategy for secured debts, where you whip out a payment plan, strike a pose, and say, “I’ve got this.”

Let’s dig into this suave priority debt repayment plan option a bit more. Imagine you’re part DJ, part tightrope walker in the bankruptcy circus. With Chapter 13, you’re spinning tracks and balancing payment plates, all to make sure that your secured assets don’t end up as scratch records in the hands of your debtors. You could potentially manage to keep your prized possessions and avoid having them repossessed. Now, isn’t that music to your ears?

So in summary, my fabulous financial friends, bankruptcy doesn’t have to mean surrendering to the rhythmless dance of debt. You can orchestrate an encore where you come out ahead, doling out the cash like a concession stand on overdrive. You hand the tax man their popcorn first, of course, and then you skillfully manage the autographs, I mean, assets, secured with collateral. It’s all part of the show-stopping performance called Chapter 13.

Handling IRS priority debts: It’s like juggling fire torches, so wear gloves and pay the piper.

Managing secured priority debts: Keep your belongings off the auction block with smooth moves and a steady plan.

Priority debts repayment: Wear your financial crown and pay those debts with a curtsy and a bow, one at a time.

Bankruptcy strategy for secured debts: It’s a high-stakes game of keep-away, and you’re aiming to score big by keeping your assets close to your chest.

And there you have it. Rolling out the red carpet and navigating the bankruptcy ball while clutching your belongings tight might seem daunting. But with a little finesse and a lot of savvy planning, you might just exit stage left with a standing ovation from the audience—and your assets intact. Checkmate!

How to Handle Priority Debts in the Maze of Bankruptcy

Picture this: you’re in the thick of navigating bankruptcy, feeling like a mouse in a labyrinth with the cheese always seemingly just one turn away. Here’s where knowing how to handle priority debts matters—it’s like having a map to cut through the maze. These debts are like your Aunt Edna during the holidays: ever-present, and you just can’t shake them off. But there’s hope—even Aunt Edna nods off eventually.

Now, imagine you’ve got a bankruptcy financial strategy that’s slicker than a greased pig at a county fair. Chapter 13 lays out a debt repayment plan that’s the equivalent of Santa’s list—everyone gets their share in order of importance. Priority debts? Those bigwigs are right up there at the front, belly-up at the buffet, ready to take a large bite out of your wallet.

Here’s a nifty trick: balance your income against your outgoings, like a circus performer spinning plates. You’ve gotta be meticulous. It’s the linchpin in how to craft an effective debt repayment plan. Sure, it won’t be the sexiest budgeting you’ve ever done, but it might just keep you from performing the bankruptcy boogie.

Creating a timeline can work wonders for keeping those pesky priority debts in check. Draft up a schedule where you’re paying Uncle Sam for that overindulgence at the tax buffet first, then chip away at the rest, spreading payments as evenly as your butter on morning toast.

Debt Type

Chapter 13 Strategy

Expected Outcome

IRS Debts

Create a rigorous, front-loaded payment plan

Become the IRS’s golden child

Alimony & Child Support

Ensure full, timely payments in the plan

Stay out of legal hot water, peace of mind

Criminal Fines

Prioritize these over other unsecured debts

Transition from financial fugitive to model citizen

Secured Debts

Utilize Chapter 13 plan to catch up on arrears

Waltz away with your car keys and home under your arm

Understanding how to handle priority debts is not just good sense, it’s an art form. It’s about split-second decisions, like defusing a time bomb while juggling hand grenades. You’ve gotta be swift, precise, and oh-so-careful. Believe me, the last thing you want is to be doing the tango with the bankruptcy court because you stepped out of rhythm.

Use Chapter 13 to your advantage—dance the dance, stick to your budget like it’s your dance partner, and let each dollar shimmy and shake its way to the right creditor’s purse. Do this, and you just might sashay through the bankruptcy fiesta, leaving with nothing but sighs of relief and maybe, just maybe, a little confetti in your hair.

Conclusion

So there you go! As our rollicking excursion through the world of Priority Debts in Bankruptcy winds to a cheeky end, it’s clear that these financial VIPs are not just another hoop to jump through on your bankruptcy journey. They’re more like the ring of fire at the circus—thrilling, a tad dangerous, but ultimately a part of the show. If you thought getting a fresh financial start was going to be a simple trot around the board game of life, guess again. It’s more akin to a madcap game of Twister—with the IRS as an inflexible player hogging all the red dots.

While meandering your way through this fiscal forest, it pays to remember that not all debts are created equal. Yep, priority debts are like the squirrels gathering nuts for winter; they’ll snatch up what they’re owed before the non-priority nuts ever get a look in. But chin up, dear reader! With a sprinkle of savvy and a dash of determination, navigating these treacherous waters could see you sailing towards the sweet shores of overcoming financial hardship.

So, lace up your boots tight for this bankruptcy journey, because it can feel like a hike through the unknown with a backpack full of rocks labeled ‘debt’. But with a compass pointing towards understanding priority debts, you might just find that you’re tougher than you think—that you can emerge from this tempest tussle with a fresh financial grin. And with that, you’re ready to slam the door on debt’s face and strut into your future with a little less financial weight on your shoulders. Ain’t life grand?

FAQ

Will understanding priority debts give me an edge in my bankruptcy case?

Absolutely. Knowing who the heavy hitters are in your debt lineup is like holding a map in a treasure hunt. By understanding priority debts, you’re better equipped to navigate through the twists and turns of bankruptcy. It’s like having a strategy guide in a labyrinth, leading you toward that precious fresh financial start. Knowledge is power, especially when you’re trying to negotiate the rocky terrain of paying off debts.

What’s the strategy for dealing with secured priority debts when I’m bankrupt?

Dealing with secured priority debts is like having a rock and a hard place as your dance partners. These debts have collateral, like your house or car, and if you don’t pay, the lender can snatch them away. The smart move, especially in Chapter 13, is to shimmy into a repayment plan where you catch up on past payments and keep your toys in your sandbox.

What’s the deal with IRS priority debts during bankruptcy?

Ah, the IRS. Imagine it as the determined collector who never forgets to show up when money’s on the line. IRS priority debts are tax obligations that the government insists you pay. Think of it as a persistent reminder that Uncle Sam always wants a slice of the pie, even when you’re trying to divvy up a smaller financial plate.

How are priority debts different from non-priority unsecured debts in bankruptcy?

Think of priority debts as the guests with a backstage pass—first dibs, no questions asked. Non-priority unsecured debts are like fans with general seating. They’re waiting in the wing with slim chances of seeing any action if the priority debts have their way. These include credit card debts, medical bills, and personal loans, which typically have no collateral and hang out at the back of the line in the bankruptcy buffet.

Can you break down the difference between Chapter 7 and Chapter 13 bankruptcy for me?

Sure! Imagine Chapter 7 as a giant garage sale where your assets are sold off to pay creditors — like a clearance event for your debts. It’s the clean-sweep approach. Then there’s Chapter 13, which is more like a makeover for your finances. You get a court-approved budget and a repayment plan. Think of it as going on a financial diet and working out a plan to get back in shape over three to five years.

What are priority debts, and why do they get special treatment in bankruptcy?

Priority debts are like the royalty of the bankruptcy world—they jump to the front of the payment line because the law says they’re super important. They include things like child support, alimony, certain taxes, and fines. The court gives them the red-carpet treatment because they’re obligations that society deems non-negotiable. So even though you’re broke, these are the debts that get paid before the others can even think about getting a penny.

How do I handle priority debts in bankruptcy without losing my mind?

To handle priority debts without joining the circus, you’ve got to become the ringmaster of your own financial revival show. With a solid plan, usually in the form of a Chapter 13 repayment strategy, you evenly distribute your available dough among your tenacious creditors, tackling the most insistent debts head-on. It’s all about balance, timing, and staying on top of your money game.

What exactly falls under the category of priority debts in bankruptcy?

Priority debts are the VIPs that include heartstring-tuggers like child support and alimony, along with the party poopers like criminal restitution and certain tax debts. These are the ones that will stick to you like gum on a shoe, demanding full payment even as other debts might be wiped clean or reorganized.

Sorting through the horror of my credit cards in bankruptcy kinda feels like a laugh track in a sitcom gone wrong. Hit the dramatic tunes, because contemplating personal bankruptcy feels like the grand finale no one saw coming in my financial saga. Picture this: the cherry on top of a chaotic five-year divorce, a whirlwind of debt accumulation, and a relentless army of unpaid credit card bills that just kept piling up. These bills, born from a mix of divorce delays and lost clients during a global pandemic, became the bane of my existence, threatening to erase any trace of my once-thriving career.

As I flirt with the idea of venturing into bankruptcy court, I imagine it less as a leap into the abyss and more as an intrepid exploration of a haunted house, where the scares are more predictable than petrifying. In this mental walkthrough, my credit card debt stands on the brink of its final act under the stern gaze of Chapter 7, ready to take a bow and exit stage left. On the flip side, Chapter 13 unfolds like a structured plan, a steadfast ally that offers a strategy to combat my debts without the need to escape the financial specters lurking beneath.

So, to anyone out there gripping their credit card statements a bit too tightly tonight, take heart. While the prospect of filing for bankruptcy might not conjure up visions of fairy tale endings, it might just be the unexpected plot twist that paves the way to a sequel filled with promise, financial stability, and the chance to start afresh, free from the chains of credit cards in bankruptcy woes in 2024.

A credit card debt assessment before diving headfirst into bankruptcy can be the vat of acid superhero origin stories are made of.

Don’t get spooked by terms like “Chapter 13” – it’s a structured payment plan, not a haunted hotel room.

Debt doesn’t have to be a four-letter word; bankruptcy can be the start of your financial happily ever after.

Anecdotes from DubG’s Debt Diary: The Reality of Sinking in Credit Card Debt

Imagine my wallet as a deck of cards, each one concealing the joker that is my looming debt. Engaging in financial tug-of-war post-divorce, with credit cards as my dubious weaponry, became my dreaded daily duel. As the months slipped by, the weight of my bills loomed like a series of unfortunate events that seemed far removed from the hilarity of a sitcom scenario. Navigating Credit Card Debt in Bankruptcy was a concept that, at the outset, felt like capitulating to my nemesis: the overwhelming debt narrative.

The cascade of expenses mimicked a magician who pulls not a rabbit but an unending scarf of bills from his hat, each statement sneering with anticipation for funds I knew weren’t there. Recognizing my narrative aligned with many credit card debt relief experiences, I saw bankruptcy as a last resort—a diving platform into an uncertain abyss that promised to cut my Achilles’ debt.

Amid my high seas of debt, it was the personal bankruptcy filings that tossed a lifebuoy in my direction, offering glimpses of a possible fresh start. The fact that American debtors found relief through $2.03 trillion discharged in bankruptcy from 2009 to 2018 shines a beacon of hope on my financially capsized boat.

Yet, the stigma associated with such a financial reset is as persistent and annoying as a popcorn kernel lodged in one’s teeth during a movie marathon. Despite this, tearing off the ‘scarlet B’ off one’s chest proved to be a remarkably savvy move, a sleight of hand granting indebted souls a debt disappearance act unprecedented by any magic show.

Creditors’ relentless pursuit akin to a horror movie chase scene

A judicial restraining order on said monstrous collectors

Interest rates soaring like eagles, preying on my fiscal carcass

A possible freeze on the carnivorous compound interest

Assets hanging by a thread over the pit of liquidation

A shield for some possessions under certain bankruptcy chapters

So as I penciled each number into the mounting pile—part algorithm, part epitaph—I trudged forth, clutching onto the remaining fragments of humor as my prospective financial life preserver. The thought of casting these digits into oblivion through bankruptcy started transitioning from a distant pipe dream to an actionable path. Debt, much like my collection of bad jokes, should eventually get the boot—preferably out of a cannon.

Understanding Bankruptcy Options: Chapter 7 vs. Chapter 13

So there I was, at the crossroads of financial redemption and ruin, pondering the existential question: to Chapter 7 or not to Chapter 7? Or should I dance with the devil known as Chapter 13 debt restructuring? As I mulled over my bankruptcy options for credit card debt, it became clear I needed a plan—a robust strategy that didn’t involve flipping coins or consulting a Magic 8-Ball.

Let’s talk Chapter 7 bankruptcy insights, shall we? Imagine if your financial burdens did the Houdini and disappeared—now that’s music to anyone’s ears. Chapter 7 waved its wand and promised to make my credit card debts vanish. The black cloud of asset liquidation, though, hovered ominously. Could I bear to part with my prized collection of novelty coffee mugs? A conundrum, indeed.

Enter Chapter 13, the knight in shining armor for folks clinging to their worldly possessions, offering a proverbial Monopoly ‘Get Out of Jail Free’ card. Payment plan development is the heart of Chapter 13, reminiscent of a financial diet that could slim my hefty credit card debt without the fear of my vintage vinyl collection being auctioned off to the highest bidder.

Breathe in the fresh air of financial clarity with the following table that juxtaposes the two bankruptcy personas:

Chapter 7 Bankruptcy

Chapter 13 Debt Restructuring

Credit card debts potentially wiped clean

Credit card debts slimmed down in a payment plan

Assets hit the chopping block

Possessions secured tightly like Spandex

Income qualifies as ‘Not a Rockefeller’

Steady income needed like morning coffee

Over and done faster than a TikTok video

A 3-5 year financial marathon, not a sprint

Each bankruptcy option felt like stepping into an alternate financial universe. Although Chapter 7 flirted with my desire for a clean start, the potential asset forfeiture was enough to make my wallet weep. Chapter 13, on the other hand, demanded discipline and a tryst with a court-dictated budget—think extreme couponing without the thrill of the hunt.

Decision time echoed with suspense, yet equipped with the right bankruptcy knowledge, I was ready to make the call—time to level up from a debt-ridden damsel in distress to a financial phoenix rising.

What’s the Difference Between Secured and Unsecured Debts?

In the battlefield of finances, debts are the invisible landmines waiting to explode. They come in two flavors: secured and unsecured. If my assets were a castle, secured debts would be the trebuchets, threatening to dismantle the very walls I hold dear if I default. My car, for example, secured by a finicky acquaintance called an auto loan, might be towed away into the sunset should I renounce my payment duties. And my home – my personal fortress – could face a similar soul-crushing fate in the hands of the mortgage lender; talk about property collateral risks!

Unsecured debts, the rogues of the debt world, lack any claim on my worldly possessions. They’re like those annoying flying monkeys in my financial Oz – no claws in my coffers but malevolent enough to command my attention. And let’s talk about the ringleader of this unsecured shindig: credit card debt. Like a master of ceremonies at the most unwanted financial circus ever, credit card debt categorization often determines how fiercely I’ll grapple with my wallet’s nemeses.

So, when the bankruptcy bell tolls, it’s the differentiation between secured and unsecured that comes to the rescue, deciding which creditor takes a haircut and who’s left holding the comb. Below, is an exposé on how these debts stack up in the bankruptcy arena, with a nod to asset protection strategies that might just save the day:

Secured Debts

Unsecured Debts

Property—as hostages to the cause

Only my promise to pay stands guard

Failure to pay may result in a silent auction of my treasures

They huff and puff but can’t blow my house down

Collateral at stake, like a plot twist in a melodrama

Asset-stripping drama, unlikely my friend

Bankruptcy could be like playing chess with my beloved items

Discharge potential: as high as my deserted island dreams

And there you have it! The delectable dichotomy between the debts with dominion and those without. In the former, my prized possessions serve as pawns; in the latter, they’re immune to the fiendish whims of credit card companies – oh, joyous reprieve!

So, before hoisting the white flag and surrendering to bankruptcy, knowing your enemy is half the battle. Know thy debts, secure your knowledge arsenal, and may the asset protection strategies be ever in your favor!

Navigating Credit Cards in Bankruptcy

Here’s the skinny on managing credit card debt in bankruptcy: it’s like a GPS for your wallet — only instead of avoiding traffic, you’re dodging financial potholes.

Down the Chapter 7 route – ‘The Clean Slate Expressway’ – you could see your credit card debts do a Houdini, disappearing faster than my motivation on a Monday morning. But remember, credit card debt discharge in bankruptcy has its own rule book: No funny business with racking up debt pre-filing. That’s like wearing a ‘Kick Me’ sign at your own trial for fraud prevention in bankruptcy filings.

Jumping onto the Chapter 13 ‘Payment Plan Parkway’, your debts might get trimmed like a bonsai tree. While the interest rates halt their ascent to the stratosphere, teasing out that budget over a 3-5-year extended remix means you’ve got to shuffle those dollars like a Vegas card dealer under the court’s eagle eye.

But either bankruptcy path lands you at a Destination: Silence. As in, calls from credit card companies go from ‘Daily Annoyance’ level to ‘Glorious Silence.’

Still curious how this looks on paper? Feast your eyes on this tableau of credit card debt settlement strategies:

Chapter 7 Freedom Fiesta

Chapter 13 Payment Party

Debt likely discharged into oblivion

A structured fiesta of finesse, paying off debt bit by bit

Asset surrender may be on the menu

Cling onto your assets like a rodeo rider

Qualification based on income vs. debt showdown

Put that income to work, like it’s chopping wood

Expedited conclusion, like a binge series with only one season

Patience is required — it’s the ‘Lord of the Rings’ extended cut

When it comes to navigating the labyrinth of credit card debt in bankruptcy, it’s about weighing the options, doing the legwork, and maintaining a trapeze artist’s balance between tactical discharges and strategic repayments. And always, always, avoiding those sneaky pitfalls of fiscal shenanigans that could have you labeled a bankruptcy fraudster.

Conclusion

Think of bankruptcy not as a financial Grim Reaper, but more of a pit crew at the Daytona 500 of life’s fiscal racetrack. This isn’t about towing your economic jalopy into the junkyard; it’s about showing up at the garage, toolbox in hand, ready to work on credit card debt consolidation in bankruptcy. When the rubber hits the road, that’s when you’ve got to bite the bullet, turn that key, and drive down the highway toward a fresh financial start post-bankruptcy.

And let’s squash the notion that filing for bankruptcy is akin to pressing the self-destruct button on your financial life. On the contrary, it’s like hitting the reset button on an arcade game. Suddenly, you’ve got a fresh set of lives and the scoreboard’s been wiped clean. Sure, the ghosts chasing you down in Pac-Man may represent your creditors, but this time, you’ve got a power pellet called the bankruptcy code benefits. With a bit of strategic financial planning and a touch of legal maneuvering, you’re back to chomping down on those pesky dots of debt.

So whether you sprinted into debt with the speed of a gazelle or it crept up on you like a sloth with a mission, remember: bankruptcy is your financial pit stop—an opportunity to refuel and swap out those bald tires of past financial missteps for a set of slick new wheels. Hit the road with a tune-up and a clear destination, and who knows, the next pit stop could be your victory lap. Onward to solvency, my friends!

FAQ

How can bankruptcy lead to a fresh financial start?

Bankruptcy can hit the reset button on your finances. Imagine shaking off those credit card debts like a bad ex. Post-bankruptcy, you get a clean(ish) slate to rebuild your credit and make better money moves. It’s like financial spring cleaning, but you might need to follow a strict budget afterward to keep your house in order. Hello, financial zen!

What should I understand about managing credit card debt during bankruptcy?

Managing credit card debt in bankruptcy is about strategy—think chess, not checkers. You need to understand the rules of discharge to get ahead. And, remember, no funny business like going on a shopping spree before filing—that’s a big no-no and could get you in trouble for fraud.

How do secured and unsecured debts differ in the context of bankruptcy?

Secured debts are like that friend who holds your favorite sneakers, hostage, until you pay back that $20 you borrowed. If you don’t pay, they take your stuff. Unsecured debts, like credit card debt, are more like a nagging parent—they can’t take your stuff, but they sure can make life miserable. Bankruptcy tends to be kinder to you with unsecured debts.

What are the main differences between filing Chapter 7 and Chapter 13 bankruptcy for credit card debt?

Think of Chapter 7 bankruptcy as the ‘nuclear option’—it’s a clean slate but can liquidate some assets to pay off debts. Chapter 13 is more of a structured diet plan, where you repay a portion of your debts over time without losing all your stuff. Your income and assets play leading roles in determining which option suits your financial saga.

Can you share any personal anecdotes about dealing with overwhelming credit card debt?

Oh, where do I start? Credit card debt can mount up faster than my failed attempts to cook a Thanksgiving turkey—just ask my smoke detector. When you’re buried in debt, those little pieces of plastic in your wallet feel like ticking time bombs. I’ve personally been there; it’s like your own financial horror show, where every statement is more terrifying than the last.

How is credit card debt assessed in personal bankruptcy filings?

In personal bankruptcy filings, credit card debt is typically treated as unsecured debt. This means it can usually be discharged or forgiven, depending on the type of bankruptcy you file for. Chapter 7 may obliterate this debt completely, while Chapter 13 might require a repayment plan.